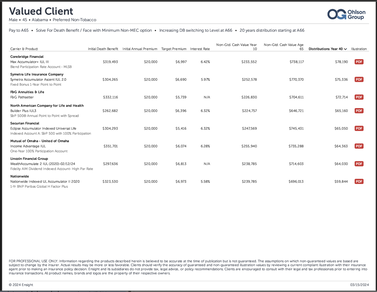

The conventional approach to designing accumulation-focused Indexed UL strategies involves minimizing the death benefit. Often, this is combined with using the maximum AG49 compliant illustrated rate to squeeze every dollar of projected income out of the product. While that can produce a compelling illustration, it may not be the most effective approach in the real world. That thought process is often the reason for things like stress testing or reducing the illustrative rate, even if it results in a reduced illustrative income. The truth is there is another, perhaps more meaningful alternative design that can deliver more consumer value from virtually any Indexed UL product. This more balanced approach to case design can deliver:

What's the Bottom Line?An additional $248,387 in coverage, an increase of over 61% versus a traditional design. The product includes a Chronic Illness ABR that is now based on a 61% larger face amount, putting more cash at the client’s fingertips when they need it most:

Over $14,000 in additional funding capacity per year. Remember, all the testing that limits how much premium you can contribute “rolls” forward. By the 10th policy year there is a whopping $140,000 of additional funding capacity. What's in it for the Advisor?As the face amount increases, so does the Target Premium. Using this consumer value packed approach increases Target Premium by 61%. What Products Work with this Approach?This strategy likely works with the majority of accumulation focused IUL products. Case design will be a manual process. Increasing the face amount from a maximum accumulation solve by 50% might be a good starting point. Need a hand creating illustration examples for your prospects? Contact the Life Department at Ohlson Group. We will help put your case together and provide supporting marketing material and case submission / and underwriting assistance. Download a Male 45, Preferred Non-Tobacco PDF Flyer

0 Comments

We all know that FIA’s provide tremendous upside potential and protection from downside risk. We have all (rightfully so) preached to our clients and prospects that “zero is your hero!” What if you had an FIA product whereby you could tout, “Four is Your Floor?” A new hybrid MYGA/FIA product is now available and allows you to provide a minimum guarantee of four percent with an S&P 500 strategy that gives your client a 90% participation rate. Pretty amazing story to tell your clients. Oh yeah, that participation rate is locked-in for seven-years… What a great way to start a conversation with a prospect or an existing client. “Mrs./Mr. Client, I have a financial vehicle that allows you to participate in 90% of the S&P 500 for seven-years and participate in NONE of any losses that may occur. In fact, the worst-case scenario would be a 4% annual return!” Ladies and Gentleman, today’s annuity rate environment may be as strong as we’ll ever see. Virtually any existing client or annuity owner is a hot-prospect. Asking for a meeting to discuss Refinancing their Retirement has been netting great results with several of our agents. Even if the prospect’s existing annuity has surrender penalties, many carriers are understanding and realize that most clients that purchased an annuity during the low interest rate environment could fare much better by switching to a newer FIA with better rates and more upside potential. Need help presenting this concept? Have questions about a case you’re working? Contact Ohlson Group today at 877-844-0900 and let’s talk!

To say that we live in interesting times would be an understatement. The public has so much access to information, and there is such a push for transparency. Are there easy steps you can take to amplify your business? The answer is yes. You must get a little introspective and make a commitment to follow a mini-plan. Let’s take a look at these steps:

STEP 1 - Find a specialty that you really believe in, excel in, and are ready to commit to. To say that you are in the “financial services business” may just be a little too general, as everyone is in this arena. If you establish credibility (believability) as a retirement income professional, then we have narrowed things down. But maybe you should be a financial services specialist, focused on the retirement income and maintenance needs of Americans. Specialists make more sales, make more money, and obtain more referrals. STEP 2 - Add to your product mix. Maybe it’s time to offer index annuities with lifetime income benefits, MYGAs, and Wealth Transfer/SPL with chronic illness benefits to hit the top 3 needs of baby boomers. STEP 3 - Get online. If clients and prospects cannot find you online, you will have a rough time convincing them that you are the “go-to person” we described in step 2. An IMO should have the resources to assist you and give guidance in this area. If they don’t, then try googling insurance marketing organizations or field marketing organizations until you find a firm that can help you. If your “favorite” IMO does not appear on the first or second page, then, as the song says, “You better shop around.” STEP 4 – Have a website that is truly… a different experience for the consumer. Make the site a place full of useful information that your prospects and clients enjoy visiting. Have videos, whitepapers, and consumer info sites available. Sound like a tall order? It depends on what IMO that you work with. STEP 5 – Get involved in your community. Sponsor a ball team, have a booth at an author’s luncheon, be seen at places where your target prospect goes, and do educational meetings. Let them know, through membership in the Safe Money Places Agent Network, that you have the support and assets of a large National organization while remaining an independent advisor focused on the needs of your clients. Sort of like “think global, act local.” In summary, this can all be done rather quickly if you are working with the right IMO, have the desire to “step it up,” and are serious about improving your practice.  Some agents always seem to be successful, while others struggle to keep their heads above water. This occurs regardless of the economic climate, product line, or market segment.

Are they superhuman? Were they born lucky, or do they possess extraordinary sales skills? Do they know something you don't? Well, they might have some special skills and talents, but that's not the secret. What is the secret? The main difference is having a plan—not just a marketing plan, but a business plan as well. Successful advisors run a business and a financial services practice. They are not merely product salesmen who thrive when markets are favorable. They have a plan and understand their past and future trajectories. However, yesterday's successes are over, and it's time to move forward. Successful advisors are NOT product salesmen. Product salesmen are successful when things are hot. They are attracted to low hanging fruit. They are not professional business planners. The pros, on the other hand, know where they are going and where they have been. That may be the most important part of the planning process. Successful advisors embrace turmoil and this is when great advancements are made. Anyone can make good money in easy times. Turbulent times bring out the best in the top producers. They do two very important things. They listen and learn. They listen to the public’s needs and concerns and seek out ways to satisfy these challenges. They read, attend classes and develop new strategies. They become counselors as opposed to sales people. They refine their skills and prioritize fundamentals, setting them apart from their competition in the long run. In conclusion, most never made claims as to how they can have you triple your business in one year. Most advisors spoke to their constituents about staying in the game, building a business that would stand the test of time, and most importantly, doing it with credibility and integrity. So, after this diatribe, what am I suggesting to be the answer to success? Hard work is of course a primary ingredient. People skills are extremely important. But, at the foundation of success is the plan and the people that help you develop and implement your program. In short, “plan your work and work your plan.” That’s what we are doing right now.  Any agent that has been selling annuities for even a short period-of-time knows that not all first-year index strategy rates are what they seem. Many an agent have horror stories of carriers providing a shiny first-year cap rate – only to have their stomach drop a few years later when opening a renewal statement showing a 30%-50% drop in their client’s cap rate. The worst part is having to go back and explain to the client why this happened. Now, this is the name of the game – that is what many in the industry have told me. However, that does not have to be the case any longer. We have a carrier that has a cap lock guarantee. Meaning, on anniversary, the carrier is contractually guaranteed to renew the cap at the initial cap rate you sold your client. That cap rate is 10%! That is 10% today and 10% for the entire length of the surrender-charge-period. Often, I ask myself, “why isn’t every agent in America selling this product?”. I looked in the mirror and realized I am not getting the message out clearly enough. So here it is – as simple as I can put it … Lock It in At 10%! Give us a call and we can turn your renewal rate nightmares into sweet dreams for you and your client base! Until Next Time – Good Selling!

In my thirty-plus years of experience in this business, I've observed that many advisors overlook asking their clients the most crucial questions. The art of data gathering, once masterfully taught in the early days of the career agent, has seemingly lost its prominence. Back then, successful marketing packages led to significant insurance and annuity sales, all rooted in thorough question-and-answer sessions.

The concept remains simple to this day: the more we understand about a prospect and their needs, the better service we provide and the greater the potential for a successful sale. This approach also fosters the development of long-term clients rather than mere customers. So, why do advisors neglect to refine their "fact-finding" skills? I believe much of our failure in this regard stems from our society's obsession with instant gratification. We often chase trends or follow the latest fads without deeply considering our clients' true desires and objectives. While some clients benefit from a product switch that offers higher interest rates or a more substantial death benefit, is that truly aligned with their financial aspirations? Have they given thought to questions like "How much money do I need?" and "What do I want my money to achieve for me?" Perhaps it's time to revisit this fundamental aspect of the sales cycle. Could there be an opportunity to embrace traditional practices in a modern context? I believe so. Our prospects and clients are bombarded with information, mostly delivered in sound bites. Many consumers, after making a purchase, find themselves somewhat dissatisfied, despite feeling they've improved their situation. This dissatisfaction leaves them open to other advisors' approaches, making repeat sales and quality referrals harder to come by. As a result, we find ourselves investing more time and money in one-off sales. So, what's the initial step? Allow me to suggest asking just two questions before completing the client questionnaire:

These questions spark open discussions about their financial concerns and aspirations. Armed with this insight, you'll be better positioned to offer tailored solutions for the present while planning for the future. After all, we know that benefits sell better than features. When clients realize that you genuinely address their needs, wants, and desires, you'll establish yourself as the trusted advisor in your market. This is yet another facet of service: caring. People want to do business with individuals who genuinely care about them.  Undoubtedly, there are clients with enough assets to pay for care should they need it later in life. That said, this may be one of those instances where just because you can, doesn’t mean you should. More often than not the decision to self-fund is due, at least in part, to not wanting to think about the possibility of needing care. It also completely omits the planning component by focusing strictly on the funding.

In terms of funding, simply transferring this risk to an insurance company is going to provide a significant discount. What is often not factored into the decision to self-fund, however, is the impact of taxes. Unless paying with cash from a checking account that doesn’t accumulate interest, every time the client liquidates an asset to pay for their care, they are creating a taxable event. At either capital gains or ordinary income rates, the tax burden this creates can grow quickly. There are additional factors that can make this a more significant problem:

Some might think that the taxes can be offset by deducting the cost of care. Maybe, but maybe not. There are two complicating factors here:

So, what’s the moral of the story? Self-finding only makes sense if the real cost of the approach is superior to an insured solution. That determination needs to include all contributing factors to the cost of both self-funding and an insurance solution. Fortunately, there are ways to mitigate the taxes that may be triggered by either approach. In the case of an insurance solution, things like the Pension Protection Act and case designs with extended premium payment durations can be used to minimize or even eliminate taxes at the time of purchase. In the case of self-funding, finding loss harvesting and other strategies can reduce the net taxes due. The crux of the matter is asking a very simple question of those who plan to self-fund: Have you thought about which assets you will use to fund care, and did you consider the tax ramifications of your strategy? The subsequent conversation may point to an insurance solution more often than you think.  While the recently passed SECURE Act 2.0 is generating quite a bit of conversation in retirement planning circles, it has not had near the impact in the life insurance segment that the original SECURE Act did when it was passed back in late 2019. The primary impact of SECURE 1.0 in the life insurance space was the significant change to Stretch IRA rules, making inherited IRAs even more of a tax challenge for beneficiaries. Read on to learn more about a strategy to work with both G1 and G2 for a comprehensive solution!

In an ironic twist, planning opportunities stemming from SECURE 1.0 focus not as much on the taxes paid by “G2” beneficiaries, but on the “G1” IRA owner who has had the good fortune to accumulate a large qualified plan balance and the ability to fund a traditional IRA Maximization strategy involving current distributions to fund a life insurance policy with far more favorable tax treatment. This presents some planning obstacles for all involved, including:

This last issue, the remaining balance inherited by G2, has two components:

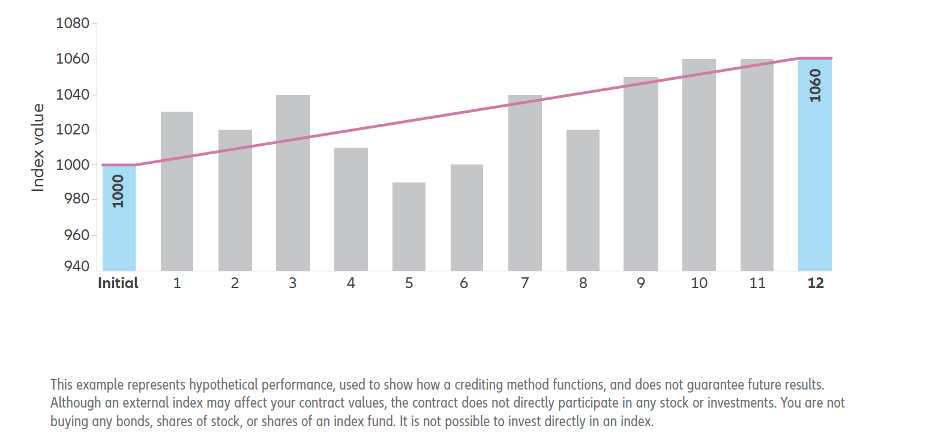

Fortunately, many of the challenges listed above are easily solved with a life insurance strategy focused on G2. By establishing a permanent life insurance policy as part of G2’s retirement planning approach, there is the possibility of avoiding the taxes that would be due on gains from other asset types. This policy is funded by a portion of the inheritance, and are a number of design elements to consider to render it maximally effective: Consider using a face amount in excess of the minimum required to accommodate the portion of the inheritance allocated to the strategy. The “balanced” approach to the design will also increase any amounts available via accelerated benefit provisions included in the base policy or added via rider, strengthening G2’s care planning strategy. Availability of participating loans early in the policy could allow for higher funding levels, subsequently using a policy loan to pay taxes when due in April of the following year, versus holding a portion of the proceeds back in anticipation of future taxation. Another consideration is one of timing. While the fact that there is a future inheritance may be known fairly early on, the timing of the event is obviously unknown. This could present a problem if there are insurability issues for G2 that present themselves at the time of the inheritance. The solution to this challenge is to put the insurance in force on G2 early in the process, in anticipation of the future inheritance. Doing so eliminates insurability as a future unknown and would also become part of G2’s overall retirement planning. Having a tax-favored source of retirement income above and beyond the ability to accommodate the inheritance strengthens the resilience of their overall retirement plan. If this approach is pursued, the use of a policy face amount higher than the minimum required for G2’s premium budget at inception creates the capacity to accommodate the future inheritance. While this strategy has been described as a way to solve the issue of not being able to execute a traditional IRA Maximization strategy, the use of these two strategies in concert would be maximally effective in terms of reducing taxation of the IRA and minimizing G2’s tax burden on a forward-looking basis. This “second sale” to G2 in an IRA Maximization strategy can also be used to prospect up or down the family tree, depending on where the original client relationship lies. PUT US TO WORK ON YOUR NEXT CASE!  Fixed index annuities (FIAs) have many strong advantages to help protect your client’s savings and provide sustainable income over many years. Our goal is to help you gain a better understanding of the components that make up FIAs. This knowledge will enable you to make well informed decisions when it comes to product selection and design. FIAs accrue interest based on an external index, the index selected determines the amount of indexed interest received, which will fluctuate based on index change over the crediting period. The choice of the external index stands paramount. It is critical to explore the array of index options aligned with your FIA considerations. Equally crucial is the selection of the interest-crediting method for your FIA. The crediting method determines how fluctuations in the index will be calculated then credited to the annuity. The method chosen incorporates elements such as caps, spreads, and participation rates, which may greatly impact of indexed interest earned. In the subsequent sections, we delve into prevalent crediting methods, shedding light on how they work. Annual Point-to-PointA straightforward crediting methodology, annual point-to-point hinges on comparing the index value at two distinct points in time. This option could work well during periods of higher than usual mid-year volatility. Process Overview:

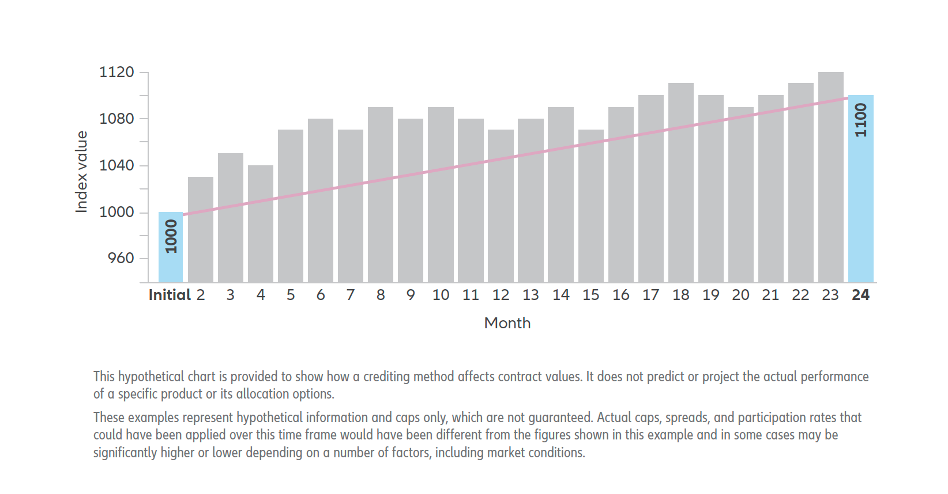

Illustrative Example: In a hypothetical scenario, if the ending index value surpasses the initial value by 6%, the indexed interest for the policy year could be contingent upon factors like a participation rate of 110%. Thus, the indexed interest would amount to 6.6%. However, if a cap is in place and is lower than the 6% increment, the indexed interest would be capped accordingly. Similarly, if a hypothetical scenario features a 3% spread, the indexed interest would be 3% (6% change in index value – 3% spread).  Multi-Year Point-to-PointEchoing the principles of annual point-to-point, the multi-year point to point spans multiple years, thereby diminishing the influence of market volatility between the selected points. Process Overview:

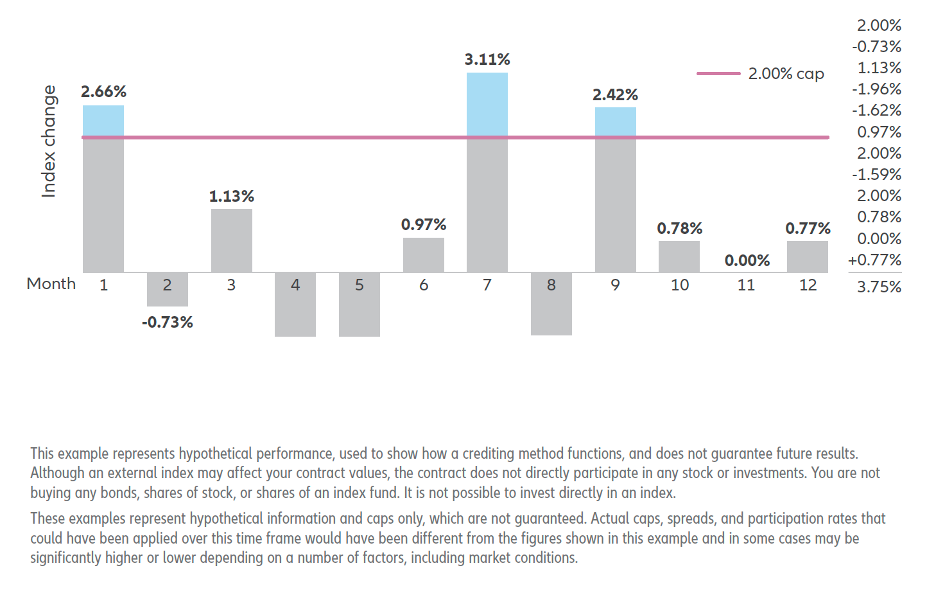

Illustrative Example: Consider a two-year point-to-point crediting scenario, where the ending index value outstrips the initial value by 10%. Assuming a participation rate of 150%, the indexed interest over the two contract years would amount to 15%.  Monthly Sum This volatility-sensitive methodology tracks monthly index fluctuations, offering interest in buoyant markets while being susceptible to downturns. Process Overview:

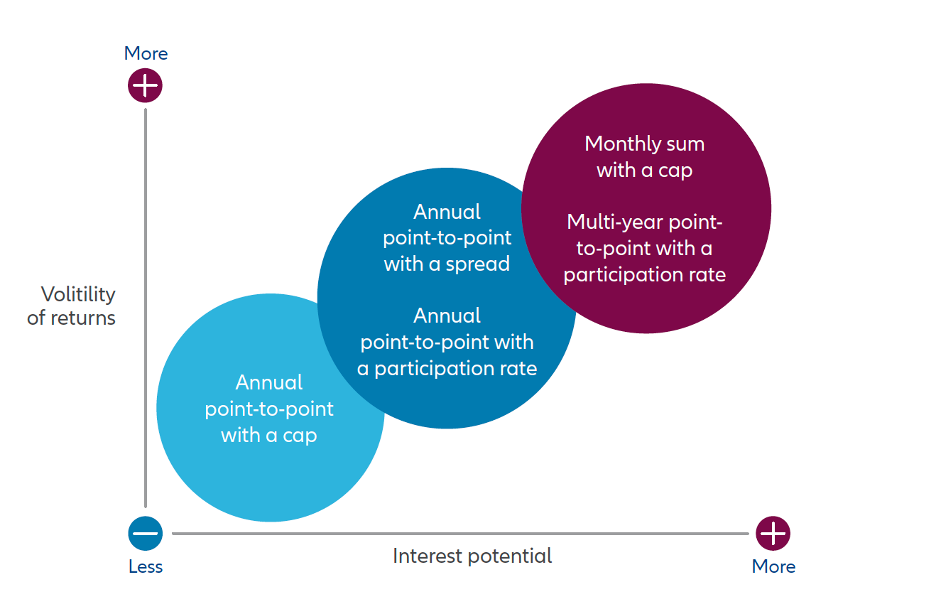

Illustrative Example: In a hypothetical monthly sum scenario with a 2.00% cap, monthly index fluctuations are evaluated. The cumulative sum determines the indexed interest, with any negative sum resulting in no interest accrual.  FIA Crediting Methods: A Quick Overview Below is a chart outlining the relative sensitivity to performance volatility and interest potential of a few common Fixed Index Annuity (FIA) crediting methods. Please note that this chart serves as a brief summary; it's essential to review the detailed descriptions of each crediting method before making a decision. Remember, no single method is universally superior. Depending on market conditions, one method may yield more interest than others—or no interest in a given year. Additionally, you have the option to combine crediting methods. Regardless of your choice, your accumulation value is safeguarded from negative performance.   When looking at net profits, money is the second of the assets that we must monitor and master. "Time" is the first asset, which you can read more on here.

I prefer to separate the money that I put into my business in two categories: Expenses and Investments. First, let’s look at and define our subset consisting of expenses and investments. Expenses are pretty easy to define. They are the basic items we need to run our practice. These are dollars spent to insure that we are able to adhere to the philosophy of Service, Credibility, Integrity and Profitability (SCIP®). Expenses are things like rent, telephone, salaries, supplies, fees paid to outside consultants, professional fees, website maintenance, business insurance, health insurance, office equipment and other things of this nature. This seems pretty straight forward but it always bares further investigation. It’s important to reevaluate your vendors at least once per year because the savings through this will increase your net profit. Expense is the biggest factor when you are trying to increase your net profit. Remember: Revenues - Expenses = Net Profit Let’s look at investments vs. expenses. Investments are costs associated with items that will either maintain or increase your net profit. Some investments must be made just to stay even and keep your flow of income. Others are dollars spent to get to the next level, such as increased advertising, website enhancement, increased direct mail, client appreciation events, new office furniture or a more prestigious location and continual education. What about a new hire dedicated to a new project? What about hiring an intern? How about hiring a public relations person to enhance your position in your community? These are investments. And there is no better place to invest in than your own business. You have the most control in this endeavor. When considering deficit spending and its possible values, just make sure you have a well thought out plan with the proper strategies and tactics to give you the best chance for success. People engage in “proper” deficit spending everyday. Kids and parents borrow money for college. Cities raise money through bonds to enhance and improve their communities. There are many more examples. Money is precious. Make sure you use it properly, for it is usually a finite asset and not never ending. |

Archives

April 2024

Categories |

RSS Feed

RSS Feed

Search Our Website to Find More Info, Tips, and Sales IdeasContact InformationOffice Address:

11611 N. Meridian Street | Ste 110 | Carmel, IN 46032 Phone: 1-877-844-0900 Fax: 317-844-4422 |

Quick Links

|

THIS WEBSITE IS INTENDED FOR AGENT USE ONLY. NOT FOR USE BY CONSUMERS.

INFORMATION CONCERNING COPYRIGHT INFRINGEMENT CLAIMS

The Ohlson Group, Inc. provides links from its website to various third party sites which may enable you to obtain locations and information outside of The Ohlson Group's control. The Ohlson Group, Inc. neither controls nor endorses such other websites, nor have we reviewed or approved any content appearing on them. The Ohlson Group, Inc. does not assume any responsibility or liability for any materials available at these websites, or for the completeness, availability, accuracy, legality or decency of these sites.

CLAIMS OF COPYRIGHT INFRINGEMENT

The Digital Millennium Copyright Act of 1998, as amended, (the "DMCA") provides recourse for copyright owners who believe that material appearing on the Internet infringes their rights under U.S. copyright law. If you believe in good faith that materials we host infringe your copyright, you (or your agent) may send us a notice requesting that we remove the material or block access to it. If you believe in good faith that someone has wrongly filed a notice of copyright infringement against you, the DMCA permits you to send us a counter-notice. Notices and counter-notices must meet the then-current statutory requirements imposed by the DMCA; see http://www.loc.gov/copyright/ for details. Notices and counter-notices should be sent to info@ohlsongroup.com. The Ohlson Group, Inc., (877) 844-0900. We suggest that you consult your legal advisor before filing a notice or counter-notice. Also, please be aware that there are penalties for false claims under the DMCA.

The Ohlson Group Inc, and or Joseph R. Ohlson LUTCF is licensed to do business in all states except New York.

Privacy Policy

INFORMATION CONCERNING COPYRIGHT INFRINGEMENT CLAIMS

The Ohlson Group, Inc. provides links from its website to various third party sites which may enable you to obtain locations and information outside of The Ohlson Group's control. The Ohlson Group, Inc. neither controls nor endorses such other websites, nor have we reviewed or approved any content appearing on them. The Ohlson Group, Inc. does not assume any responsibility or liability for any materials available at these websites, or for the completeness, availability, accuracy, legality or decency of these sites.

CLAIMS OF COPYRIGHT INFRINGEMENT

The Digital Millennium Copyright Act of 1998, as amended, (the "DMCA") provides recourse for copyright owners who believe that material appearing on the Internet infringes their rights under U.S. copyright law. If you believe in good faith that materials we host infringe your copyright, you (or your agent) may send us a notice requesting that we remove the material or block access to it. If you believe in good faith that someone has wrongly filed a notice of copyright infringement against you, the DMCA permits you to send us a counter-notice. Notices and counter-notices must meet the then-current statutory requirements imposed by the DMCA; see http://www.loc.gov/copyright/ for details. Notices and counter-notices should be sent to info@ohlsongroup.com. The Ohlson Group, Inc., (877) 844-0900. We suggest that you consult your legal advisor before filing a notice or counter-notice. Also, please be aware that there are penalties for false claims under the DMCA.

The Ohlson Group Inc, and or Joseph R. Ohlson LUTCF is licensed to do business in all states except New York.

Privacy Policy

Copyright © 2024 The Ohlson Group, Inc. All Right Reserved.